The Mind of Polycultural America: A Look at Identity, Priorities and Behaviors

October 2024

Since 2014, BBG Ventures has been looking around the corner to identify which Americans have been overlooked and underserved in health, work & education, fintech, climate, and consumer. These categories are not unique - but the vast majority of investors looking at them focus primarily on TAM and new product development. There’s no doubt that those are critical aspects of investing, but we believe that the best investment lens - and one that moves the world forward - will come from a more fulsome approach:

- A New Lens: The face of America is changing, rapidly. When we launched the firm, we first sought alpha by backing women building for women - and that will always be a foundational building block. But the past 5 years have highlighted extraordinary demographic and social shifts across race, age and income that are creating a new status quo: we call this The American Polyculture. To best take advantage of the opportunities for innovation ahead of us, investing must keep pace with the changing perspectives, behaviors and priorities of the new, multidimensional face of the country.

- A Broader View of FMF: Founders who reflect this new mix will have a competitive advantage. Founder market fit lives on two vectors: learned and lived experience. There’s no doubt that classic “learned” or professional background can qualify someone to win, but we believe that “lived” experience – the intangibles that make a founder deeply identify with, and understand, their target market – can provide an unfair advantage.

We’ve always believed that identifying which Americans are underserved and which founders understand them best will drive outsized alpha: from April Koh at Spring Health to Joanna McFarland at HopSkipDrive, from Nick Ornitz at Topline Pro to Isabela Rafferty at Canela Media, we back founders addressing the biggest pain points for this polycultural population. At a time when diversity has become a dirty word, we’re leaning in and broadening the scope: the polyculture is about a diverse nation that embraces everyone, to enable prosperity and advancement for all.

On October 30, 2024, we announced our new $60M Fund II to back overlooked founders building for the polycultural future of America. Our areas of focus align with Americans' most fundamental needs: healthcare, future of work, fintech, climate and solutions for the underserved. We will continue to back founders at the earliest stage - leading or co-leading rounds at pre-seed and seed, across B2B and B2C. And, we’ll help them accelerate to Series A and beyond: as strategic thought partners who have run businesses from start-ups to public companies; and by leveraging our newly launched Operator Network, a community of world-class builders from high-growth companies to help founders get up the learning curve and make important decisions faster.

Read on for more on our thesis around the Polyculture.

Consider the moment we find ourselves in:

- Emergence of the Majority Minority: Under 18s will be the first majority minority generation: 53% are non-White1; 1 in 4 are Hispanic, and 1 in 5 are the children of immigrants.2 Gen Z is not far behind with 47% of this generation non-White. (Contrast this with Baby Boomers who are 72% White). Meanwhile, 1 in 10 (or 33M) Americans identify as multiracial – 4 times the number a decade ago.

- Aging America: While much attention has been paid to Gen Z of late, we are no longer a young nation. By 2030, Americans older than 65 will outnumber under 18s (23% versus 20%), with older Americans living longer, working longer and spending more. Over 65s are projected to account for 57% of labor force growth in the next decade.3

- Widening Wealth Gaps: Wealth gaps are widening not just across race but across worker type. American knowledge workers are earning 37% more than deskless workers, and the gap between top quintile incomes and bottom quintile incomes has increased by 53% percent in the last decade.4

These shifts suggest that we are increasingly a nation made up of a mosaic of unique segments driven by race, gender, age, and income. This is a new status quo in which identities are diverse, complex, dynamic and evolving, where many Americans identify with multiple cultures or communities simultaneously.

In our opinion, such a major shift demands a fresh look at preferences, behaviors and priorities - and sets the scene for a reassessment of what Americans need. We can no longer rely on a singular quintessential American profile to build for the country. To better understand,fundamental priorities, and how identity shapes those priorities, we surveyed over 2000 Americans across different races, genders, ages, jobs, incomes and geographies. The full analysis with charts can be found here: The Mind of Polycultural America: A Look at Identity, Priorities and Behaviors (with charts). We plan to share subsequent reports on each of the fundamental priority areas we identified and associated opportunities, but here are the five most interesting, and in some cases surprising, finds from the data:

1. The polyculture is here: Americans’ perception of their identity is complex and dynamic, driven by multiple factors.

2. Despite our oft-cited differences we have more in common than we realize: our top two fundamental priorities across race, age and gender are health & wellbeing, and financial security; followed most often by employment & education in third place. Within health & wellbeing we are near unanimous that mental health is our top priority.

3. However, underneath those shared priorities we found significant nuance between men and women; Gen Z and Boomers; AAPI or Black Americans and other races; and between White Americans and other races.

4. White Americans, Boomers, Americans earning under $100K and workers at SMB<20 are the segments that feel least served and least prioritized by government and institutions. And, White Americans feel the least satisfied and least optimistic about the future; almost 2X more so than Black Americans.

5. Boomers are the only group for whom Environmental Safety is a top 3 priority. All other age segments, surprisingly even Gen Z, ranked it as the lowest priority.

Read on for a deep dive into each of these themes.

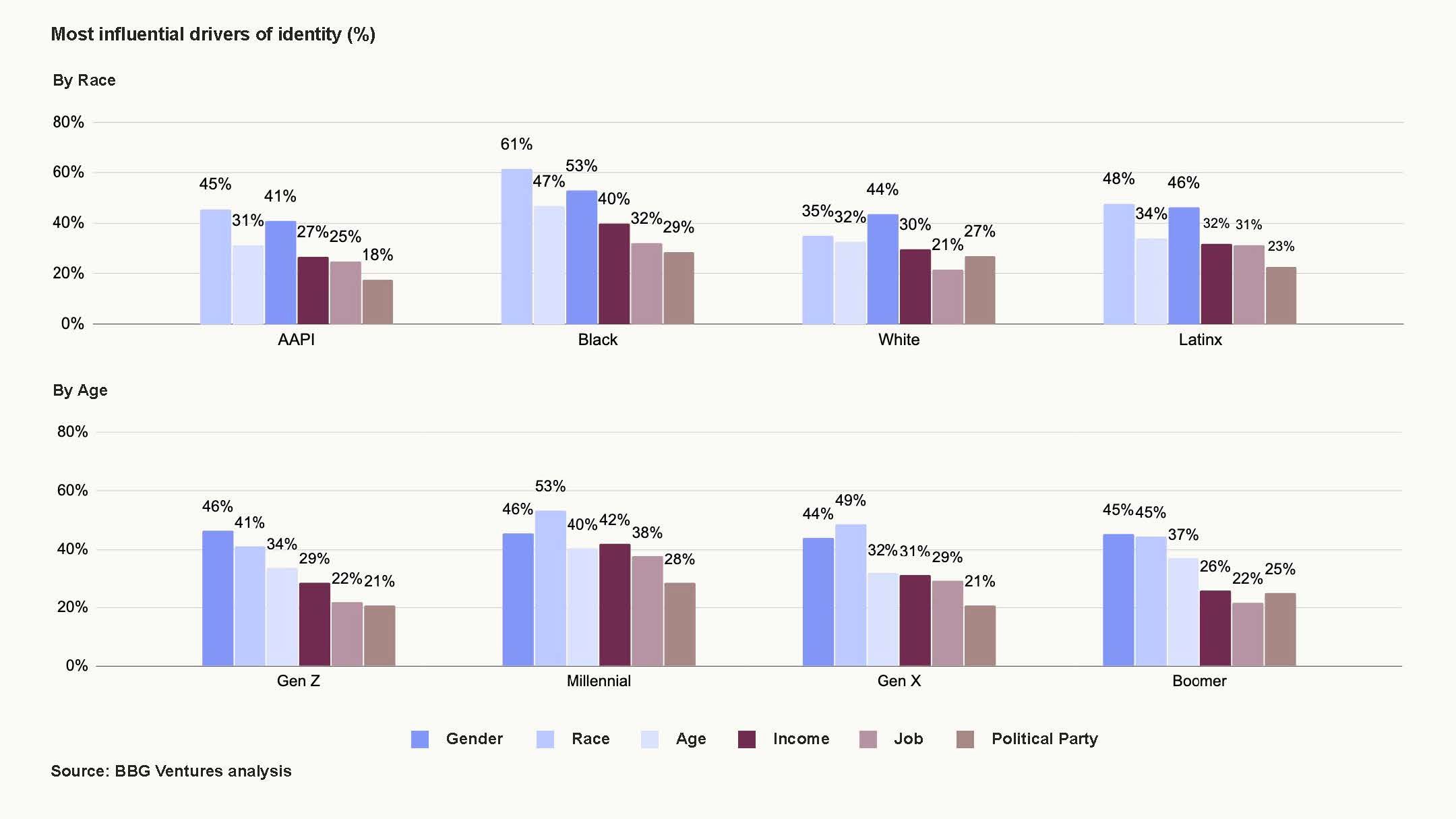

1. Americans’ perception of their identity is indeed complex and multivariate.

Our research shows that there is no uniform profile of American identity today. Each segment of the country feels defined by multiple factors - mainly a confluence of race, gender and age. By “defined” we mean that respondents consider a factor to be extremely or highly influential to their identity.5

- White Americans are more likely to define their identity first by gender (44%), then race (35%) and age (32%)

- Black, AAPI and Latinx people tend to define their identity by race first (61%, 45% and 48% respectively) then gender (53%, 41%, 46%), followed by age (47%, 31%, 34%).

- Overall, a larger proportion of Black people select these three factors as extremely or highly influential versus other groups. Income, job, and political party factor next as drivers across the races - but are of less importance. Of note: political party outranks job as the #5 factor for White people and Boomers.

- Gen Z also define their identity by gender first, though by a much lower margin than White Americans (Z: 46% gender, 41% race v. W: 44%, 35%). We posit that this may be because Gen Z have grown up in a significantly more racially diverse society. According to the last Census, 53% of under 18s and 47% of Gen Z in total are non-White, compared with 39% of the population over 18 in 47 of 50 states.7

- Other age groups ranked race first, over gender, but the story is more varied than across racial segments: more Millennials select income over age as the third defining factor; race and gender far outranked other factors for Gen X; Boomers rank political party almost as high as income as a fourth defining factor, and they are the only other segment besides White Americans who rank it ahead of job.

This has implications for founders and investors alike: Americans today are multivariate and interconnected. Meeting their needs first requires an understanding of how they see themselves, as well as what they need. Only then can we build and innovate better for the country.

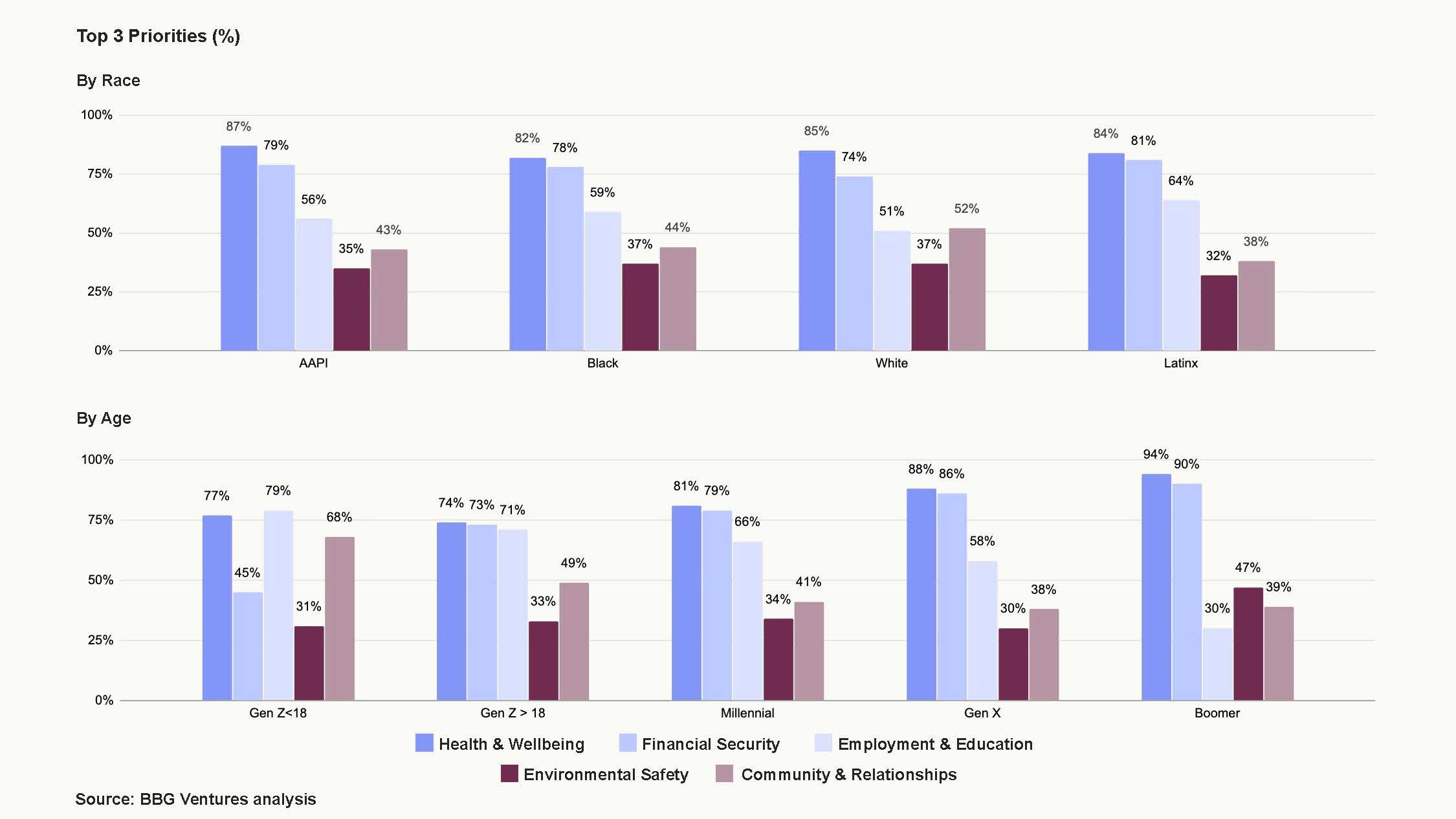

2. Despite differences, Americans have more in common than expected, presenting big opportunities for scalable solutions - particularly in health, finances and work.

Though it’s clear that Americans define their identities based on their own unique perception of their place in the world, they have surprisingly common priorities, needs and concerns across nearly all ages, races and genders.

- Health & Financial Security are the top two priorities for every race and gender, and nearly every age group (Gen Z < 18, unsurprisingly, places Employment & Education as their top priority followed by Health).

- Nearly all races rank Employment & Education as their third priority (White people marginally rank Community & Relationships as third; as did Gen Z < 18).

- Climate has the fewest people across races selecting it as a top 3 priority; and it makes it into the top three for only one age group, Boomers.

There are further shared priorities within Health & Wellbeing:

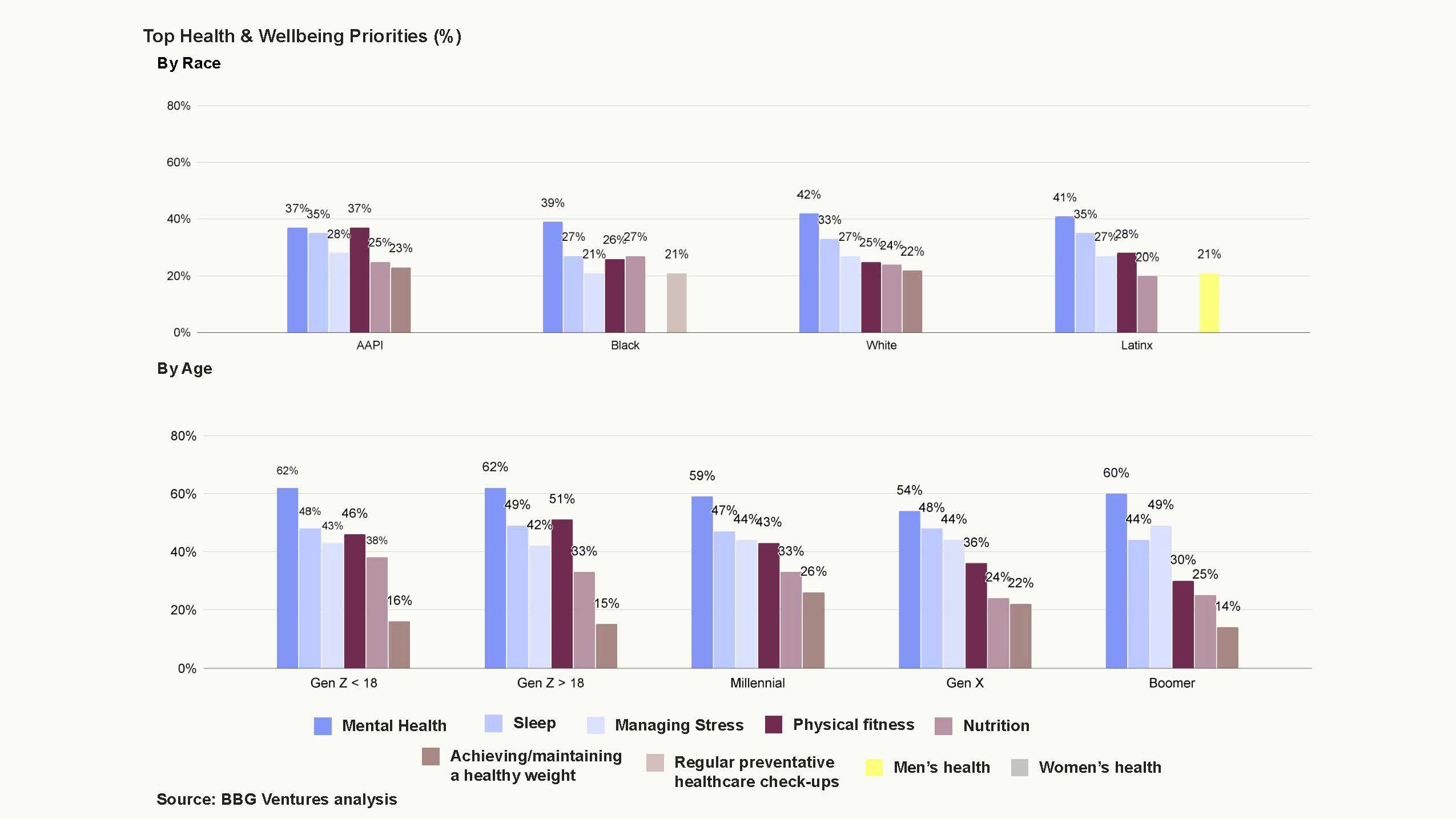

- Mental Health is the #1 concern for nearly every segment (in total, 39% of Americans) with mental health most affected by finances, stress and loneliness.

- After Mental Health, nearly every segment notes Sleep as their second highest priority (33%).

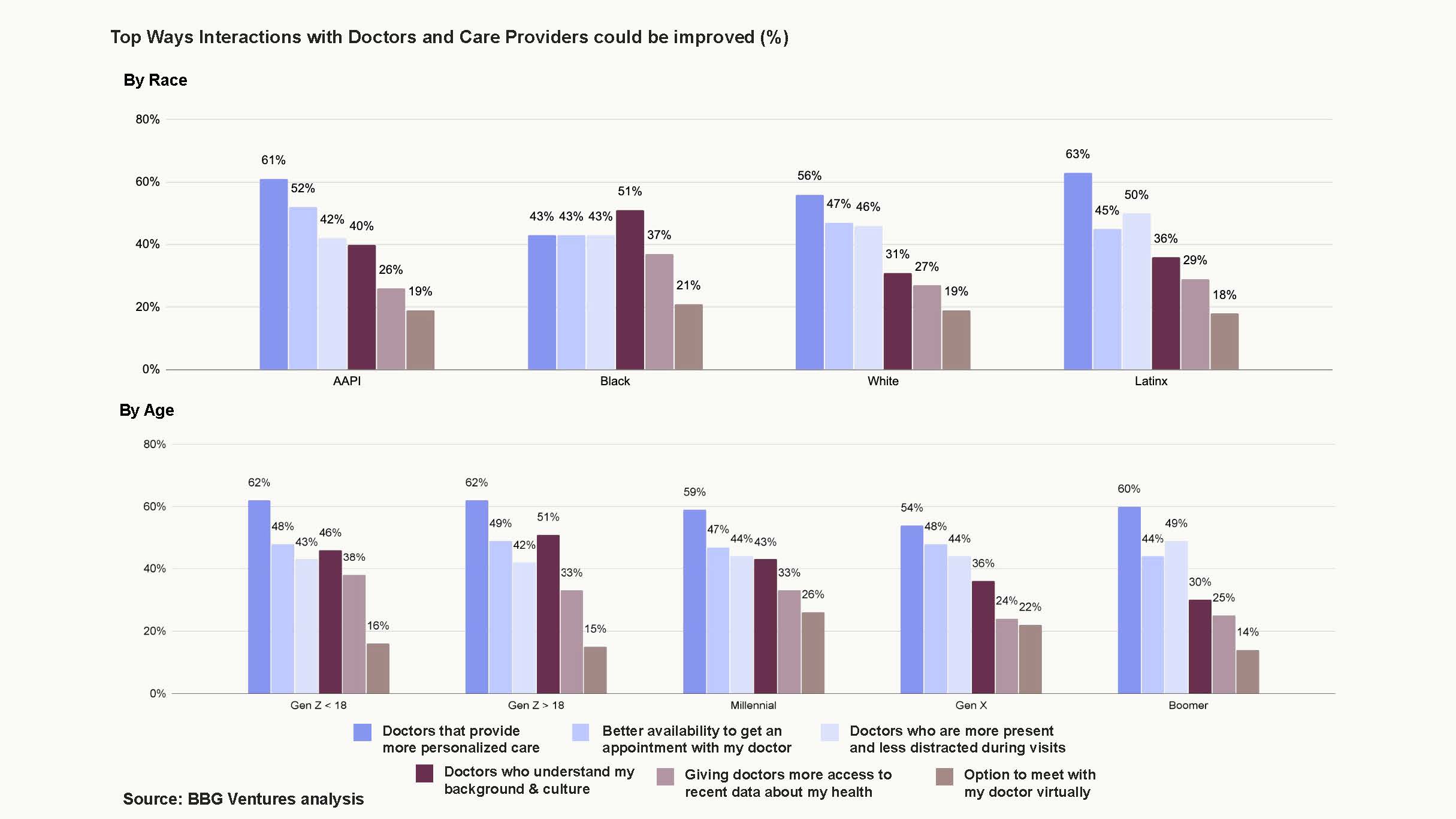

- And, while there are varying degrees of satisfaction with interactions between Americans and their doctors/care providers, there is nearly unanimous agreement on the most desired improvement: Americans want their doctors to provide personalized care, followed by either better availability for appointments or doctors who are more present and less distracted during visits. (Notably, the ability to see a doctor virtually came last for nearly all segments, prompting the question: is telehealth the savior we all considered it to be - or, is it just table stakes?)

As to Financial Security and Employment & Education:

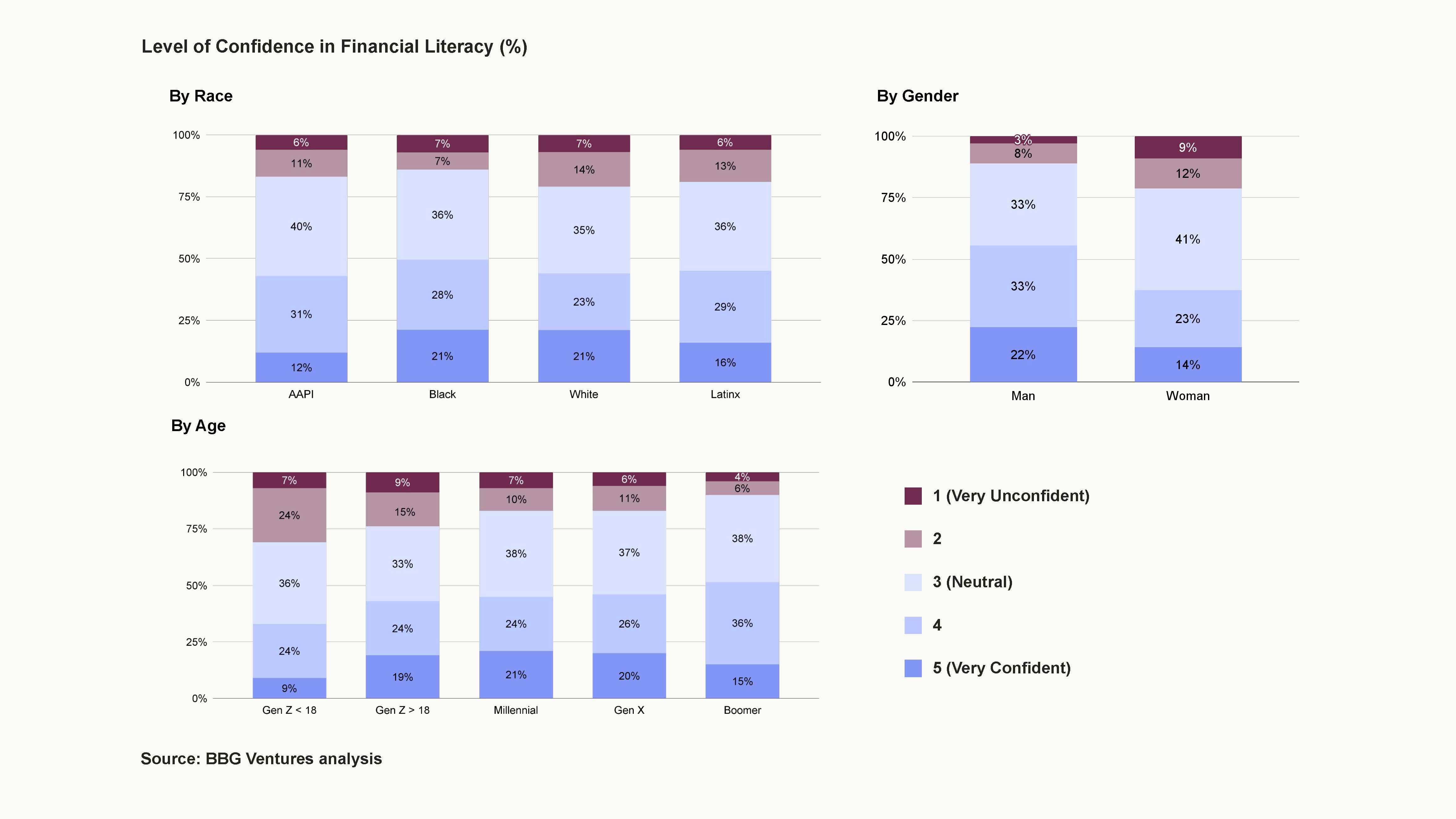

- The majority of Americans across nearly every segment lack confidence or feel neutral about their financial literacy (54%).

- Even more lack confidence or feel neutral about their financial position (65%).

- Paying bills consistently is the #1 financial goal for nearly all races and generations, followed by saving for an emergency fund. Unsurprisingly, high cost of living/inflation is the #1 factor preventing people from building wealth. This is despite the US’s so-called “superstar status” when it comes to GDP growth, historic unemployment rate lows, increasing household wealth and wage growth versus costs. Whatever the stats say, the pain of high costs is firmly planted in American minds.8

- When it comes to Employment, a staggeringly high number of employees (84%) are thinking about making a career change.9 They are considering switching jobs (37%), starting their own company (18%), taking a break (17%) or freelancing (12%); only 16% are happy in their current role. While this stat may wax and wane with the number of open jobs, it speaks to a general dissatisfaction with their current work experience and a desire for something more.10

We see two big takeaways from this high level view of commonalities:

1. While there is a ton of division reflected in news outlets and on social media, the primary concerns and greatest needs of Americans across race, gender and age are the same.

2. The emergence of America’s polyculture does not mean entrepreneurs should be building for niche segments. Common needs and common concerns suggest that the opportunity for transformative solutions is bigger than the sum of the parts.

3. Common concerns point in the right direction for innovation, but Americans’ needs are nuanced and the best solutions will be built with different groups in mind.

Identifying top priorities is only one part of the equation. Digging under the hood, the case for building better solutions by considering the needs and attitudes of each segment becomes clear. For example:

Health & Wellbeing

- Trust in Healthcare System: Americans' trust in the HC system varies significantly across both age, racial and gender segments. For example:

- 53% of Boomers trust the healthcare system versus 32% of Gen Z <18. This may correlate with our other finding that overall Boomers are more proactive about care, and find it much easier to get care than younger Americans, likely due to Medicare.

- White (22%) and Latinx (21%) Americans have a higher proportion of respondents who lack trust (“no trust” or “little trust”).

- Surprisingly, Black Americans report higher levels of trust in the healthcare system versus other races (50% have complete or some trust), driven by above average levels of trust from Black men versus Black women (59% v. 40%).

- More Black women feel neutral about trust in the healthcare system (46%), echoing a broader gender trend - overall, men have significantly more trust than women: 53% men v 39% women have “some” or “complete” trust. This is not surprising, given the lack of focus on women’s health until very recently. Women weren’t included in clinical trials until 1993 - and Black women continue to be underrepresented today. Women are diagnosed on average 4 years later than men across 770 diseases.11 Meanwhile, Black women have 2.6x the mortality rate of White women.

- Improving Provider Interactions: When it comes to improving interactions with providers, while nearly all Americans indicate they want more personalized healthcare, Black Americans (51%) prefer “doctors who understand my background and culture." This is also the second top option selected by Gen Zers (both over 18 (51%) and under 18 (46%)).

Although healthcare start-ups have begun tackling healthcare for different gender and racial segments (e.g. Tia, Maven, Mahmee) or specific concerns (e.g. Pomelo, Allara, and BBGV portfolio company Millie) we have barely scratched the surface on delivering better care and better outcomes for all Americans at scale. AI presents a huge opportunity for patient intake, integrated care, supercharging clinical decision making, as well as for optimizing provider time.

- Mental Health: Although mental health was the top priority within Health & Wellbeing across nearly every group, it is a standout for Gen Z and Millennials (53%, 46% v. 38% for Gen X). Notably, Boomers are the only group for whom mental health doesn’t rank as #1. The younger the American, the higher the proportion who rate their mental health as poor: 22% of Gen Z and 18% of Millennials say their mental health is very poor or poor, which is 2.4x and 2x respectively vs. Boomers (9%). There are clear differences in factors that negatively impact mental health: the majority of Americans report finances, stress and loneliness as drivers, while Gen Z points to self-esteem, family and school. And, while overall, most Americans turn to sleep, exercise and downtime to manage their mental health, it's mostly Gen Z and Millennials who focus on sleep as a tool to manage their mental health. Digging further we see more nuance in approach to mental health management: 1 in 5 Gen Z tries to get off social media as a panacea, whereas 1 in 5 Millennials, Gen X and Boomers look to medication. Two other key differences emerged: an equal percentage of AAPI respondents prioritize physical health as mental health. And while mental health is ranked as the #1 health priority for both men and women, 33% more women say it's their top priority. It only just squeezes into the #1 spot for men, followed very closely by physical fitness, men’s health and managing stress.

BBGV was early to mental health with its investments in broadening access to the right 1:1 therapy (Spring Health) and affordable mental fitness tools (Zeera, fka Real). Mental health then had a moment with an explosion of funding in 2020-2021 but has cooled off in the past 2 years. Funding cycles aside, the problem is only getting worse (as highlighted above) particularly amongst our youngest members. The next generation of mental health companies will need to take into account how we live our lives online and interact with younger generations in new formats. We’ve already seen unique approaches emerging, from optimizing digital wellness (Ginko) to “emotional media'' platforms (Blue Fever). We think younger founders will have unique insights on what is driving their peers’ mental health challenges and how they want to engage with their health. We’re excited to see them turn that understanding into new products and platforms.

Financial Security

- Financial Confidence: Less than half of Americans feel confident in their financial literacy (46%) and financial position (34%), but the gender gap emerges strongly here: men’s confidence levels are above the average (55%, 43% respectively), and women below the average (37%, 30%). Additionally, Black Americans (49%, 38%) tend to have higher rates of confidence versus other racial segments - particularly vs. White Americans (44%, 35%) and Latinx Americans (45%, 32%). Along age lines, Gen X (38%) is most lacking in confidence about their financial position versus other generations: not surprising, given they are on the cusp of retirement - 42% of them lack confidence that they will be able to retire comfortably. (Notably, median retirement savings for Gen X ranges from approx. $115k to $185K12 with recent reporting suggesting women have one third of that set aside.13)

- Financial Goals: Across the board, top financial goals are paying bills consistently, saving for an emergency fund, and saving for retirement; but racial differences emerge: significantly more White Americans are concerned with getting their bills paid versus other segments (57% versus 46% Black, 43% Latinx, and 37% AAPI), while AAPI are most focused on saving for retirement (47%). Meanwhile, long term investing only makes it into the top 6 for AAPI (31%) and Black Americans (20%). Notably, Gen Zers are thinking long term with investing and buying real estate making it into their top 3 goals.

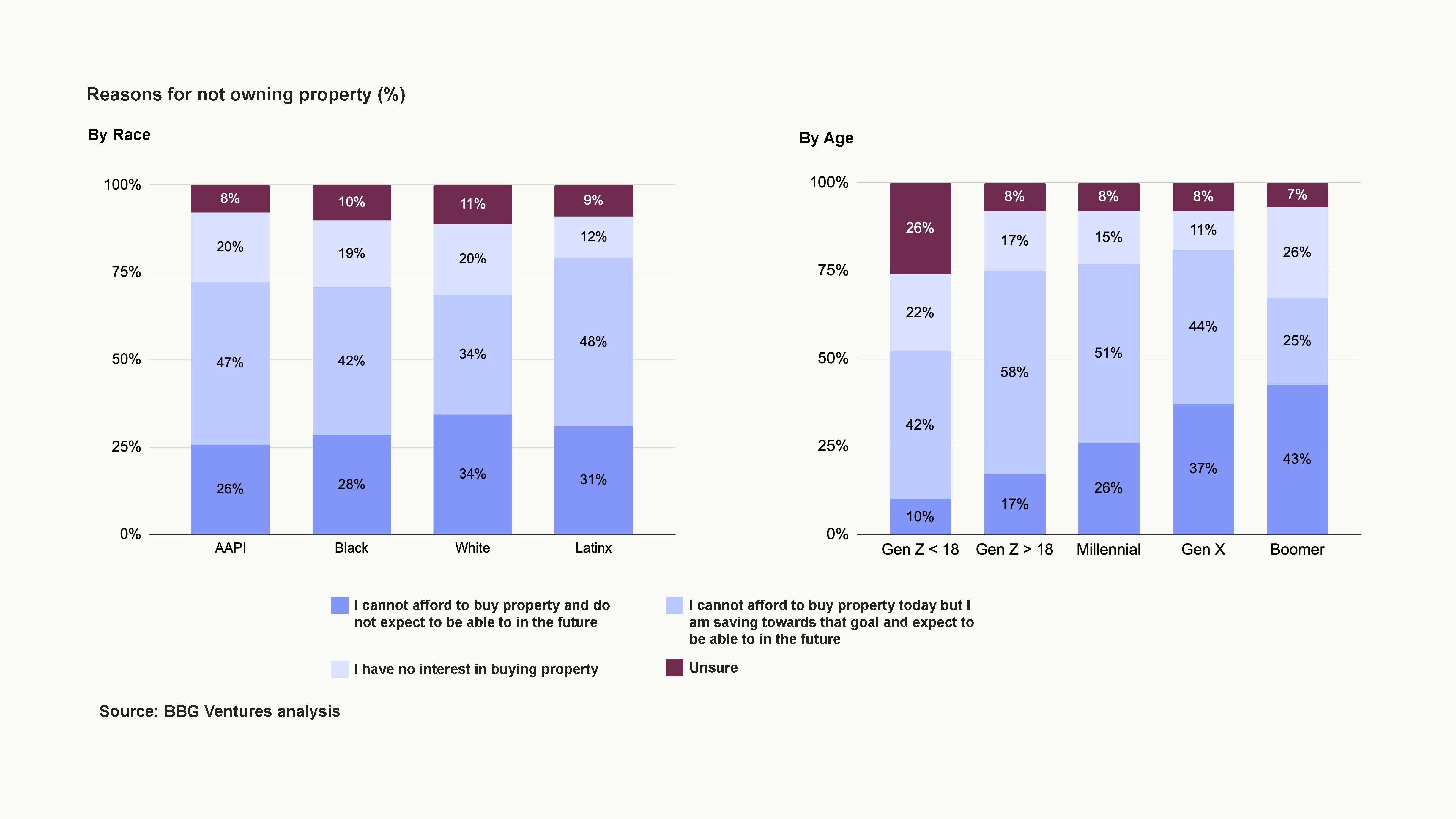

- Property: Of Americans who don’t currently own property, significantly more Latinx, AAPI and Black Americans are saving to buy than White Americans (48%, 47%, 42% versus 34%). Nearly all White Americans who don’t own property cite high cost of living as the major prohibitor (92%).

The time is now for more advanced solutions to wealth creation and management whether it’s in investing, saving or achieving financial goals such as building credit, debt management, or optimizing retirement savings. We’ve invested in solutions to help Americans increase their retirement savings (Icon Savings) and build wealth through real estate (Naya Homes). But we expect to see a step-change in innovation when AI develops the ability to assess an individual or business’s full financial picture – from dynamically underwriting credit for individuals and SMBs (Worth AI, Shubox, Hansa), to creating personalized tax strategies (Muse, April), to taking actions on behalf of an individual to optimize their financial position (Wealthmore, Monarch Money, Quinn).

Employment & Education

- Priority: While Employment and Education are the third top priority for the majority of racial groups, Black (59%), Latinx (64%), and AAPI (56%), White Americans rank Community & Relationships (52%) slightly higher.14

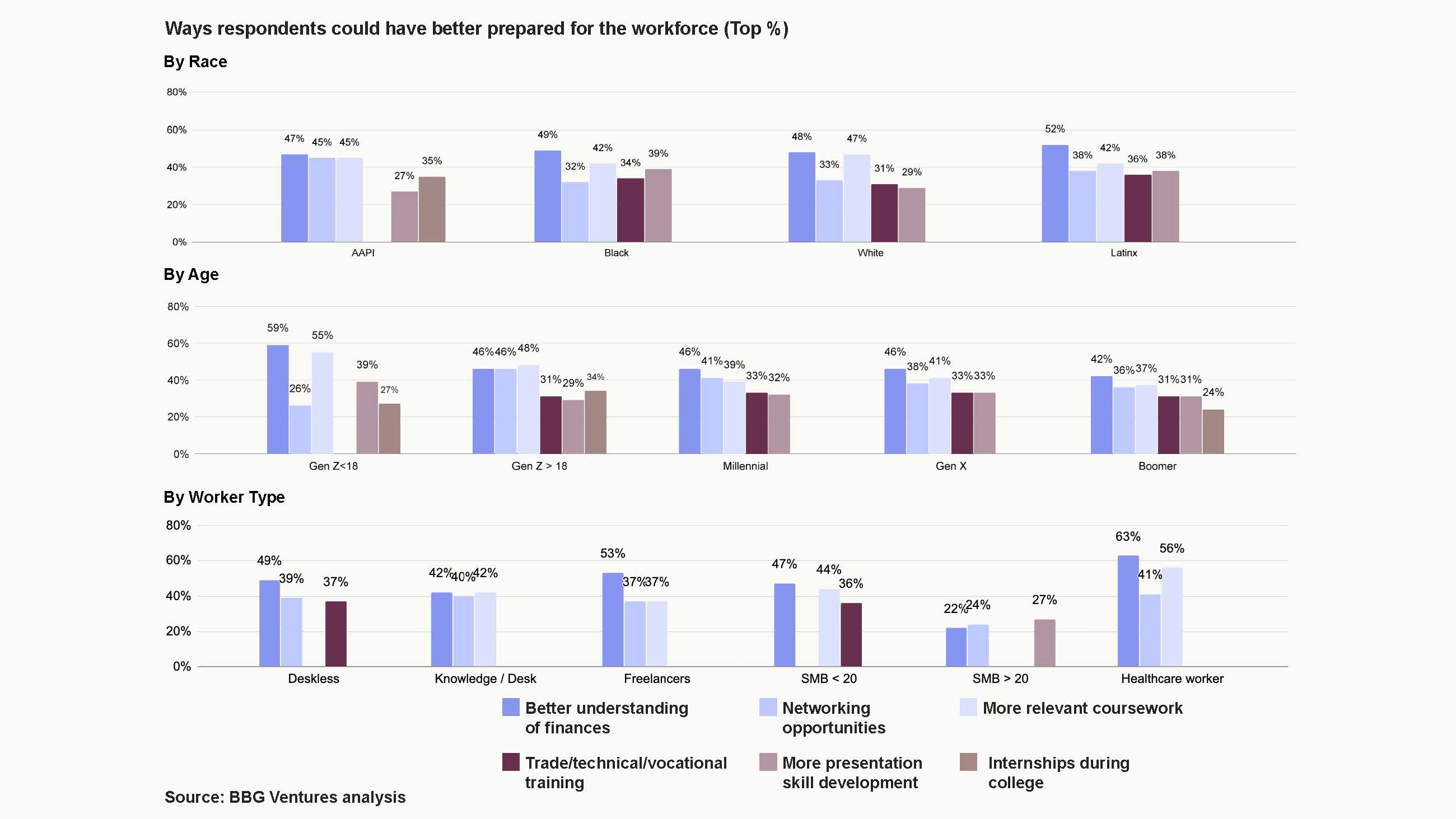

- Preparation for the Workforce: Americans generally agree that a “better understanding of finances” would have helped prepare them for the workforce (40% across all segments), followed by “more relevant coursework” (36% when looking across all respondents). Breaking it down by generation, Gen Z > 18 assigns greater weight to more relevant coursework (48%) ahead of better understanding of finances (46%, which ties with networking opportunities for second). Millennials rank networking opportunities as their second choice (41%). One note: Black Millennials opt for apprenticeship programs instead of college (39%) as their second choice behind better understanding of finances (47%).

- Career Changes: As noted above, a high number of employed Americans have considered a career change last year (84%). Of those, Black Americans prioritize starting their own companies (22%, and their top choice), followed by Latinx folks (19%, behind switching jobs). That tracks with data on new businesses opened in the US in 2023 - Latinx and Black owned businesses saw the highest growth.15

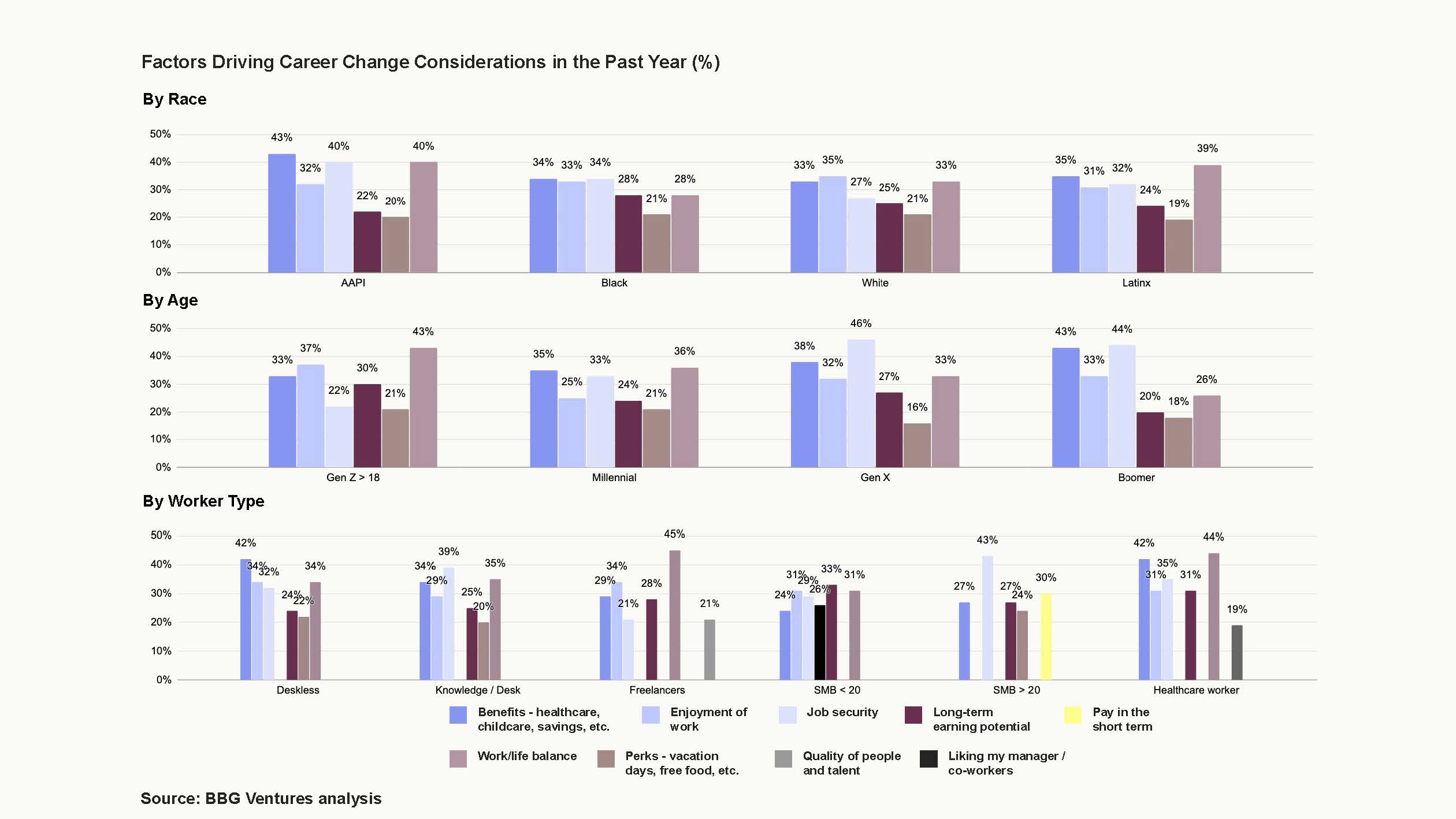

Interestingly, nearly every racial segment has different priorities when considering a new job: White Americans prioritize enjoyment of work; AAPI - benefits, Latinx - work/life balance, and Black Americans - benefits and job security. We continue to be interested in platforms that improve retention and tap into these themes, especially for deskless workers, SMB workers and freelancers who feel less prioritized (see section 4).

As for generational differences, Boomers have the highest number of respondents who say they are happy in their current role (37%). That tracks with other data we’ve seen - Pew’s 2023 research also found that +65s are happier in their jobs than other generations.16 For a deeper dive into Boomers and work, see BBGV’s Rethinking Retirement.

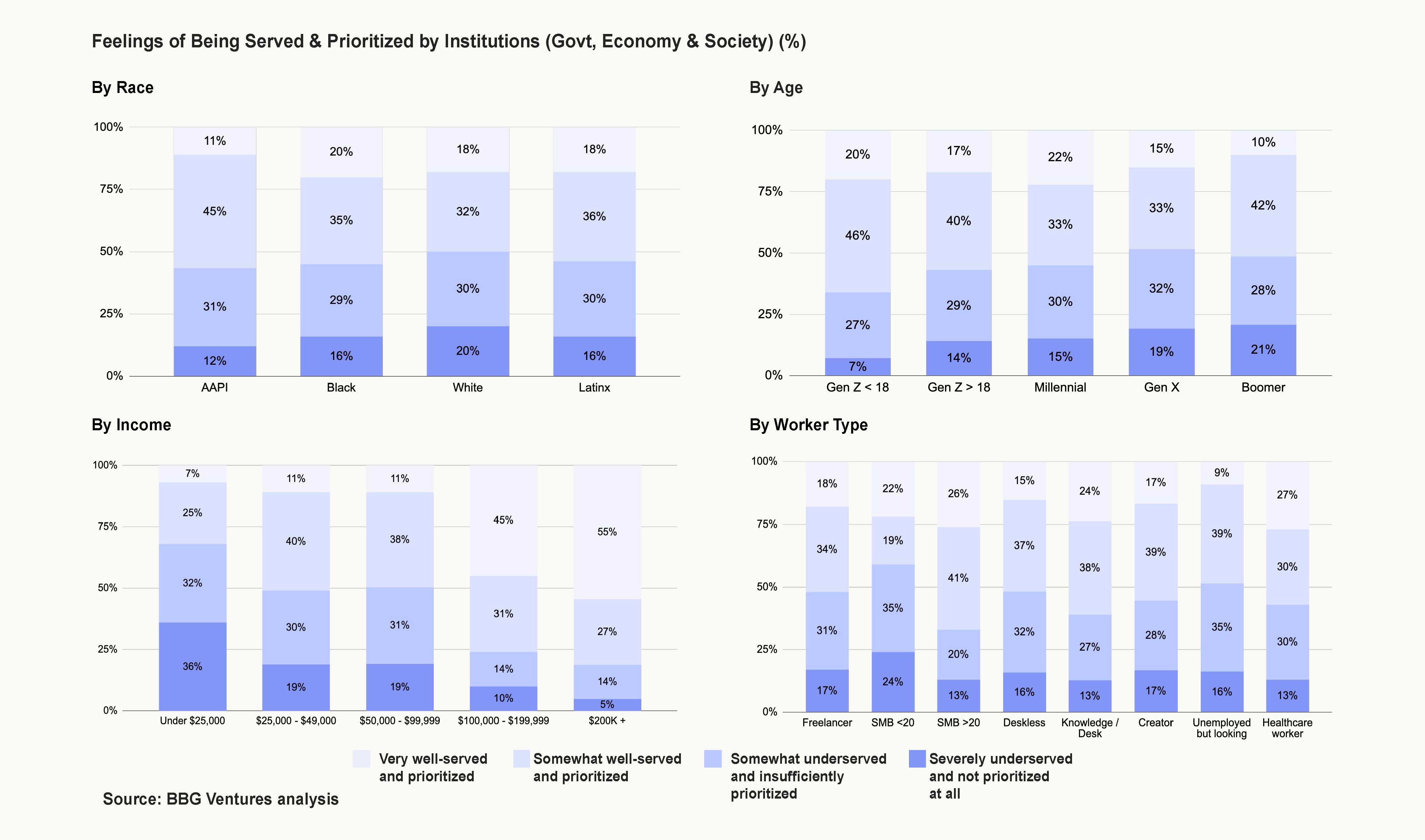

4. Overall, White Americans, Older Americans, SMB workers17 and Americans earning <$100K feel less served & prioritized by American institutions; and White Americans feel less satisfied and optimistic versus other segments.

Feeling Served and Prioritized

Generally, Americans feel split on how well they are served and prioritized by institutions (the government, the economy and society at large), but there were four groups who emerged as feeling less served and prioritized.18

- White Americans: A slightly higher proportion of White Americans (50%) report feeling “less served and prioritized” versus Latinx (46%), Black (45%), AAPI (43%) respondents. More notably, a higher proportion of White Americans (1 in 5) also say they feel “severely underserved and not prioritized at all.” This is primarily driven by two groups: 1) White Gen X and Boomers - approximately 1 in 4;19 and 2) White Americans earning under $100K - approximately 4 in 5.

- Older Americans: A higher proportion of Gen X (51%) and Boomers (49%) overall report feeling less served and prioritized, compared with 34-45% of Gen Z and Millennials.

- Americans Earning <$100K: Overall, a higher proportion of Americans earning under $100K (48%) overall report feeling less served and prioritized, compared with 28% of Americans earning over $100K.

- SMB, Deskless and Freelance Workers: Finally, feelings of being less served and prioritized also differed amongst worker segments. Americans who work at SMBs with <20 employees feel overwhelmingly less served and prioritized (59%); followed by deskless workers (48%) and freelancers (48%). The sentiment of SMB workers likely mirrors that felt by their employers, who also felt negatively impacted by the economy, according to Amex data last year. More recent data suggests that this sentiment may be turning around.20 Nonetheless there is a long record of these workers being overlooked by workflow innovation, professional development, benefits and financial security. We began investing in this space during COVID, when the nation’s two-tiered workforce of knowledge workers and deskless (frontline) workers came into stark relief. Companies like Topline Pro, Ox, Anthill, and Upwage are delivering software solutions to these previously-ignored segments.

Satisfaction

Feelings of being underserved are mirrored in responses to specific institutions. White Americans tend to be the least satisfied, and Black Americans the most satisfied.

- Healthcare: 22% of White Americans respondents say they have little or no trust in the healthcare system (versus 12% of Black Americans).

- Education: 1 in 3 White Americans say they are unsatisfied or very unsatisfied with how the education system prepared them for the workforce (versus less than 1 in 4 for other races). Of note: a similar proportion of Americans who work at SMBs with <20 employees are the least satisfied with how the education system has prepared them for the workforce (31%) followed by freelancers (26%) and deskless workers (25%).

- Financial Security: White Americans also have the largest number of respondents who report feeling unconfident or very unconfident about their financial literacy (21% versus 14% for Black people) and their financial position (37% versus 32% for Black respondents). While nearly all segments say they are focused on consistently paying their bills, it was a standout for White respondents compared with other racial segments (57% versus 43% for Latinx, 46% for Black, 37% for AAPI).

Optimism

When asked how optimistic they feel that their needs across key priority areas (Health, Financial Security, Employment & Education, Climate Safety, Community & Relationships) will be better met over the next 10 years, the majority of respondents are moderately optimistic. However, White Americans tend to be less optimistic21 (i.e. not at all optimistic or slightly optimistic) compared with other races.22 In particular, the optimism gap between White and Black respondents stands out. Black Americans have the highest number of respondents who are extremely or very optimistic compared with other races across all priority areas. It bears noting that this gap is not because of differences in income: 81% of Black respondents earned <$100K versus 73% of White respondents. We’re not the first to identify this theme: other research also suggests that Black Americans have become happier or more optimistic over time, and White Americans less.23

Digging deeper on the least optimistic respondents:

- Health: White people (18%) have 2X the rate of Black (9%) and AAPI (8%) people reporting they are not at all optimistic about their Health & Wellbeing, largely driven by older Americans and income level: 69% of these respondents are GenX and Boomers (both 34%);24 and 87% earn < $100K.

- Financial Security: White people (21%) have 2X the rate of Black people (10%) not at all optimistic about their Financial Security. Again, this was largely driven by older Americans and lower income levels: Boomers (39%) and Gen Xers (25%).25 Unsurprisingly, White Americans’ lack of optimism about Financial Security is also driven by income - 87% earn <$100K.

- Employment & Education: White people (20%) have almost 2X the rate of Black (11%) and AAPI (11%) not at all optimistic about Employment and Education. Again, this was largely driven by older Americans and income level: here 42% were Boomers; and 84% earned <$100K.

The data on White Americans feeling less prioritized, satisfied and optimistic is not necessarily a new theme, but it was surprising relative to other minority segments who are more generally considered underserved. While those gaps can’t be denied, this new data reinforces the importance of building solutions that can ultimately improve systems and platforms for all segments - and underscores income as a key driver, further suggesting opportunities to innovate around financial position and employment.

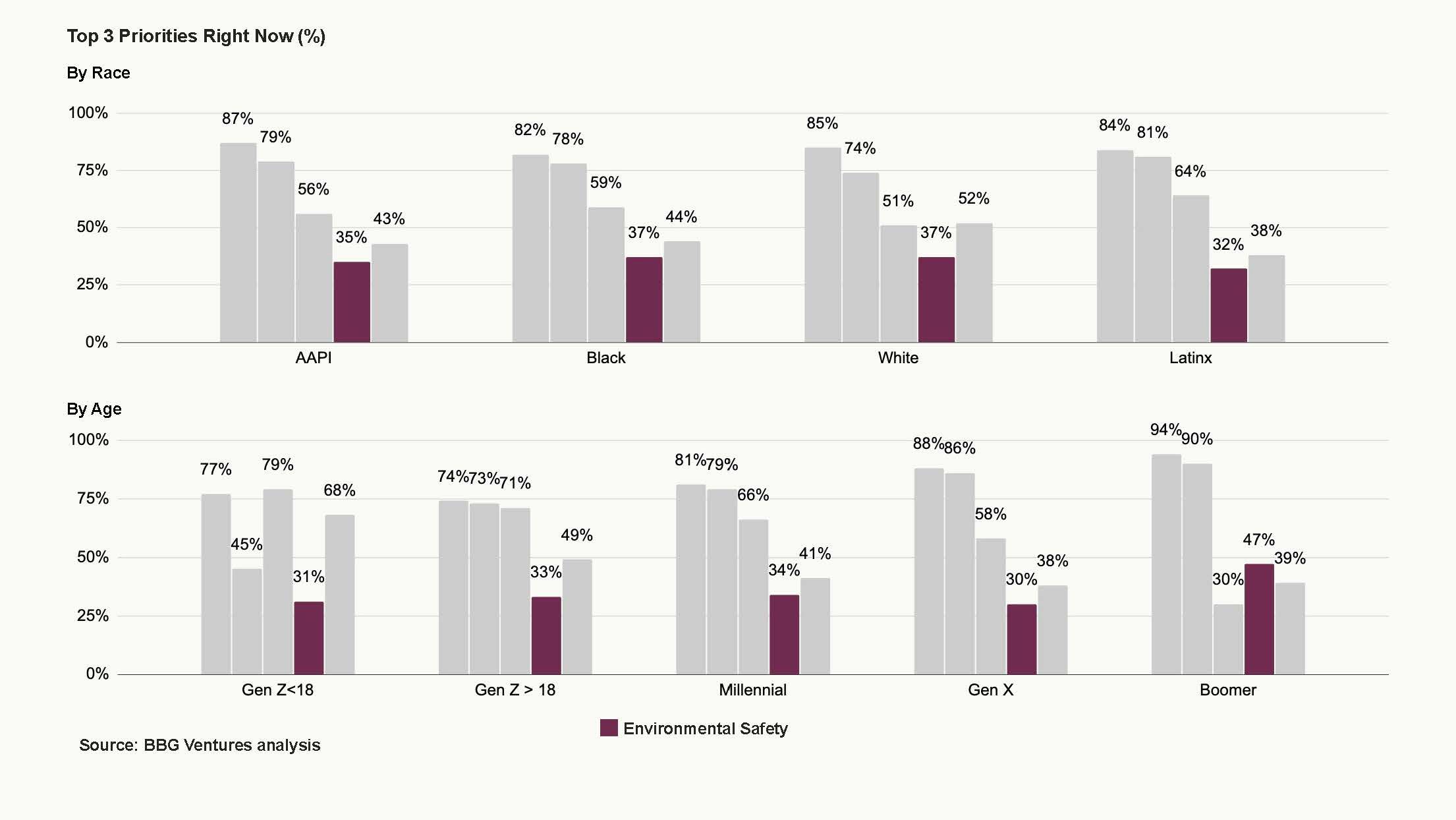

5. Boomers are the only segment across ages and races who view Environmental Safety as a top priority; but Gen Z has strong thoughts on actions required to address climate change.

Environmental Safety is a bigger priority for Boomers than other generations; 47% select it as a top 3 priority. Notably, Boomers are the only segment across age and race who say it is a top 3 priority. This is surprising given the commonly held belief that Gen Z is the loudest voice on climate change. (While roughly 1 in 3 across other age segments do say it is a top priority, this is less than half the number of respondents who selected health and financial security as a top 3 priority.)

We dug in further with those who did select Environmental Safety as a top 3 priority.26

- More Boomers (70%) state that scientific evidence is a driver of their concern about climate change versus younger people (Gen Z, 57%; Millennials, 60%).

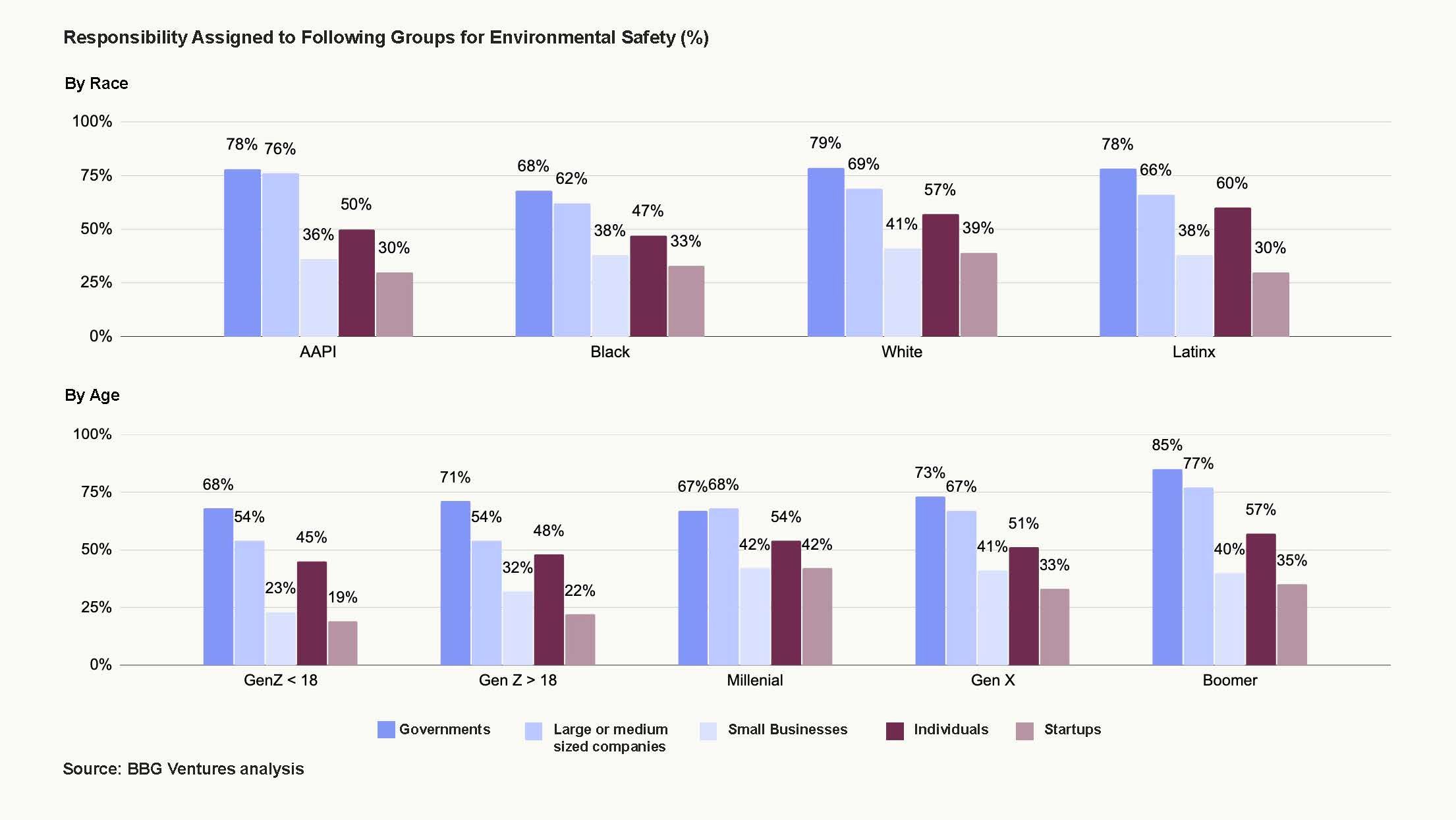

- Americans across almost all races and generations overwhelmingly believe that governments should take primary responsibility for addressing climate change, followed by large or medium-sized companies, then individuals. Millennials are the only group to assign responsibility to large or medium-sized companies about equally with governments. Boomers assign higher levels of responsibility to these groups than other generations; but notably, more Boomers also believe individuals bear responsibility versus Gen Z (57% vs. 46%).

- Americans are mixed in their levels of satisfaction with actions taken by government and large companies to address climate change. However, Gen Z < 18 are the most dissatisfied with government (46%), followed by Gen X (41%) and Gen Z > 18 (38%).

- Across the board, “minimizing waste generation, e.g. circular economy” (50%) and "transition to renewable energy” (47%) are the actions most respondents would like to see companies adopt to make them more likely to become customers – but minimizing waste is a particular standout for Gen Z < 18 (56%).

- Unsurprisingly, the majority of respondents in this section note that they have already changed their behavior to address climate change, but younger generations (Gen Z <18 (78%), Gen Z > 18 (85%) and Millennials (80%)) indexed higher than Boomers (72%), despite their prioritization of Environmental Safety. The majority of respondents are already taking a number of actions to address climate change, with “using energy more efficiently” (48%) cited by most respondents. However, when it comes to actions they would take in the future to change their behavior, Boomers and Gen X have a higher proportion of people selecting multiple actions versus Gen Z. Perhaps Boomers are more aspirational with Environmental Safety on their mind, but less action oriented in combating climate change day to day?

We’ll save a deeper dive into what we heard across segments regarding strategies and behavior change in climate safety. For now it’s worth noting that Americans largely agree that corporations need to do more to meet their net zero goals; and energy efficiency is the most agreed upon strategy that individuals are engaging in, or willing to try.

Conclusion

When we began using the word “polyculture” 2 years ago, it was off the back of an instinct around the changing face of the nation - that the country is moving beyond a quintessential American profile to a deeper acknowledgement of the dynamic and evolving nature of our society. Our research brought this to life: American identity is a composite of many parts, overlapping and different at the same time. That new, emerging complexity - buoyed by major demographic shifts across age, race, income, and worker type - presents us with a real opportunity to think differently about preferences, and priorities, and sets the stage for more nuanced solutions to our biggest areas of need: health, work & education, finance and energy solutions. If you’re building in a fundamental category, solving a big problem for all Americans, with a belief in the power of our complexities, we want to hear from you.

Addendum

Some notes on our approach:

- Notes on our survey demographics can be found below.

- We asked over 130 questions digging into more specifics around each of the priority areas, Health, Financial Security, Education & Employment, Community & Relationships and Environmental Safety - we have not included a deep dive of those in Part 1 of this report, but plan to release select insights per topic over the coming months.

- Our survey did include MENA and Native American respondents; however the sample size was too small to include them in this report.

- We haven’t addressed how Americans feel about Community & Relationships (which ranked roughly equally as the number 3 priority for White Americans and Gen Z < 18) and plan to cover this at a later date.

Methodology and Respondent Makeup

We surveyed over 2000 Americans, and we focused on cutting the data by race, age and worker type for certain sections:

- Race: 24% of our respondents identified as AAPI, 24% as Black, 24% as Latinx, and 23% as White. We also included “Native American/Indigenous” and “Middle Eastern/North African,” as an option for selection, but as the number of participants who selected these categories was much lower by comparison (< 5% and < 1%), we ultimately decided not to include these results in our final analysis.

- Age: We cut the results by generation -- Gen Z < 18 (12%), Gen Z > 18 (13%), Millennials (26%), Gen X (24%), and Boomers (24%). Used Gen Z under 18 as the best proxy we could for Gen Alpha [explain that makeup and why]

- Gender Identity: 50% of participants selected “woman,” 48% selected “man,” and 3% total selected “trans woman”, “trans man”, or “non-binary/gender queer/gender non-conforming.” Gender distribution was relatively equal across race: AAPI and White participants consisted of slightly more women (~60%), and Latinx and Black participants consisted of slightly more men (~43 women%).

- Job Type: “Knowledge/desk workers” were 29% of respondents (e.g. office or remote desk worker, executive or senior manager, and scientist) “deskless workers” were 22% (e.g. hourly workers and skilled tradesperson), “retired” were 17%, “unemployed but looking” 14%, “freelancer” made up 7%, “Healthcare Worker, “SMB < 20 employees” and “SMB > 20 employees” each made up ~3%, and “creator” made up 1%. (Job type distribution was relatively equal across race, but Black respondents were the only group to have a higher percentage of deskless workers than knowledge workers).

- HH Income: Total responses were divided along total annual household income; they ranged from “under $25k” to “$200k+,” with “25k-49k” at the highest percentage (25%), and 75% of total respondents reporting under $100k. By race, AAPI respondents had the highest percentage over 100k (25%), followed by White (21%), followed by Black and Latinx (~14%).

- Citizenship Status: Over 80% of Black, White, and Latinx respondents said “citizens by birth,” only 52% of AAPI respondents selected this option, with a comparatively much higher portion selecting “naturalized citizen.”

- Parental Immigration Status: AAPI participants also had a much higher percentage of parents who immigrated to America (61%), followed by Latinx (44%), and Black and White (11-12%).

- Language at Home: Likewise, when asked if a language other than English was spoken at home growing up, many more AAPI and Latinx people selected “yes” (~75%) than Black and White people (20%).

Footnotes

- Carsey School of Public Policy, New Census Reflects Growing US Population Diversity with Children at the Forefront; CNN, US Census Data; US Census

- Jeanne Batalova, Frequently Requested Statistics on Immigrants and Immigration in the United States

- Pew research, The Growth of the Older Workforce

- Tax Policy Center, Housing Income Quintiles; mean income gap between highest and lowest quintiles were $181,910 and $11,490 in 2012, and $277,300 and $16,120 in 2022

- Where “define” means the factor is “extremely” or ”highly” influential versus “moderately”, “slightly” or “not at all”

- Ashley Jardina, White Identity Politics; White identity politics is about more than racism - Vox

- US Census; New Census Reflects Growing U.S. Population Diversity, with Children in the Forefront

- The Atlantic, The US Reaches Superstar Status (2024)

- Only asked to people who are NOT already freelancing, running their own business, or are unemployed/retired/homemaker; equating to 88% of Americans who responded that Employment and Education was a top 3 priority

- CNBC, Nearly 50% of people are considering leaving their jobs in 2024—more than during the 'great resignation'

- Evvy, 100 Effed Facts About the Gender Health Gap

- Nerdwallet, “Average Retirement Savings By Age”; in fact, the range may be even smaller as this data is reported for ages 45-54, and 55-64

- Prudential Financial, Retirement Crisis Looming [for Women]

- Where priorities are ranked by which categories (Health & Wellbeing, Financial Security, Employment & Education, Environmental Safety (Climate Change), Community & Relationship) respondents most commonly selected as a top three priority

- Yelp, New Business Openings Report 2023

- Pew, How Americans View Their Jobs (2023)

- Workers at SMBs with less than 20 employees

- Where less served and prioritized includes respondents who selected somewhat underserved and insufficiently prioritized and those who selected severely underserved and not prioritized at all

- White Gen X - 26% and Boomers - 25%

- Amex, Small Business Blueprint (2024)

- Less or lack of optimism means “not at all” optimistic and “slightly” optimistic

- Note we saw similar trends play out across age groups and income groups more broadly across all racial segments - overall, Boomers reported lacking optimism more than other age groups; as did Americans earning less than $100K. However, White Boomers and White Americans over-indexed in lacking optimism

- American Economic Associate, Blanchflower and Oswald: Unhappiness and Pain in Modern America: A Review of Carol Graham’s Happiness For All (2019); see Fig 4

- Relative to other ages: Millennials 16%, Gen Z > 18 9% and Gen Z < 18 7%

- Relative to other ages: Millennials 22%, Gen Z > 18 8% and Gen Z < 18 7%

- 741 respondents were directed to this section based on their selection of top priorities